0

Views

Nadezhda Samkova. Work of an accountant in new constituent entities of the Russian Federation: transitional provisions, settlements with employees, reporting

Step 1. Watch the live broadcast, ask the speaker questions, take part in sweepstakes. The recording of the seminar and the test will be published after 3 business days.

Step 3. Receive a certificate After successfully passing the test, the certificate will be waiting in your personal account. You can download it and share it on any social networks.

Various formats Videos, teaching materials, checklists, online tests, sample documents and collections of regulatory documents.

Personal support Curator support for the entire period of access, as well as 24-hour technical support.

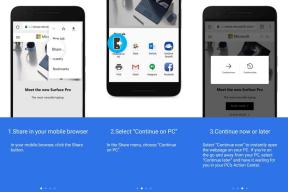

Mobile app In the application you can watch lessons and webinars, take tests and ask questions.

Nadezhda Samkova. Work of an accountant in new constituent entities of the Russian Federation: transitional provisions, settlements with employees, reporting

1. Choosing a tax system in new territories

Comparative analysis of taxation systems: OSN, simplified tax system, PSN, NPD, unified agricultural tax.

Choosing a taxation system depending on the type of activity: examples with calculations. Features of application in new regions.

Benefits when applying special tax regimes.

2. Transitional provisions

Choosing a business form: LLC or individual entrepreneur.

Features of paying taxes and submitting reports after joining the Russian Federation.

VAT during the transition period.

Inventory nuances.

Application of CCT.

3. Tax and accounting reporting

Reporting for LLC: accounting reporting, tax reporting.

Reporting for individual entrepreneurs.

General mode reporting: profit, VAT, property tax.

Reporting to the simplified tax system.

Salary reporting: 6-NDFL, RSV.

4. Settlements with employees

Nuances of the application of labor legislation during the transition period.

Insurance premiums: objects of taxation, non-taxable payments, tariffs.

Personal income tax (Chapter 23 of the Tax Code): responsibilities of agents and payment deadlines, non-taxable payments, tax deductions.

Other settlements with individuals.

Online test

Take the 5 question quiz if you want to test your knowledge.