6

Views

Young people from 20 to 30 years old often careless with regard to finance. We earn a living, spend to their needs, entertainment and hobbies, but do not even think about the rational spending of money on their budget or investment opportunities.

In fact, it does not matter how much you earn, so that investment and the calculation of the budget - it is a different attitude to money, and the number has nothing to do with it.

This post is about how to manage your finances if you get a stable salary and rarely have an income on the side.

Below you will find a description of the strategy which works perfectly even on modest salaries, as well as several tools to help you more convenient to manage your finances.

In the US, all obsessed with convenient service Mint.comIn which you can keep track of all your financial transactions.

Upon registration the user enters credit card details and can then monitor all of their using the service income and expenses, plan a budget, receive advice on cost optimization and exceeding percent notifications loans.

In our country, similar services yet. Of course, unlike the Americans, Russian consumers are not as willing to use credit cards, and in many places still do not get to pay by credit card.

Despite this, there are several convenient services with mobile applications that you can run your budget, schedule and record all expenses and receive a scheduled payment notice. I found a few free services to Russian Accounting Finance or, in other words, conducting the domestic bookkeeping.

The service, which immediately draws attention to themselves at the expense of the class name. He has a very simple interface, without any additional elements and easy record keeping. That, however, does not negate the possibility of downloading transactions some banks such as "Alpha-bank" VTB 24 and others.

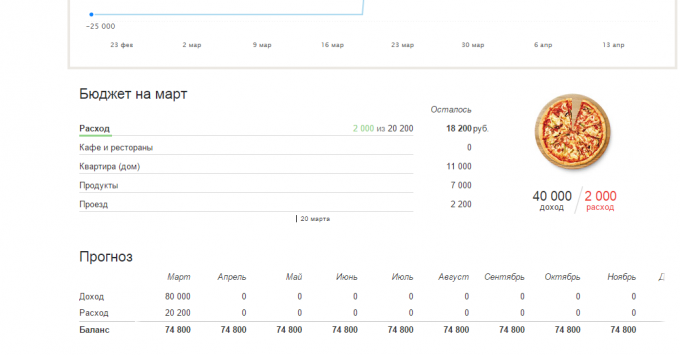

There is a built-in analytics and reports: Map of revenues and expenses, the comparison periods for debts and cash. All this in a user-friendly tables and graphs. There is also a possibility for setting financial goals, everything is pretty easy and simple.

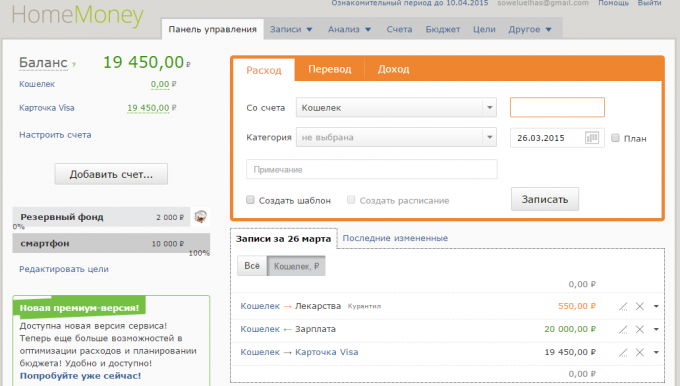

Mobile version synchronized with the Web service and includes the ability to share the family accounting, recognizes the SMS from the bank and automatically enters them into income and expenses.

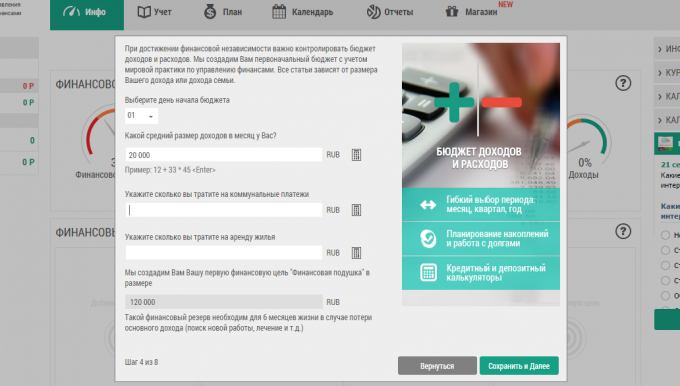

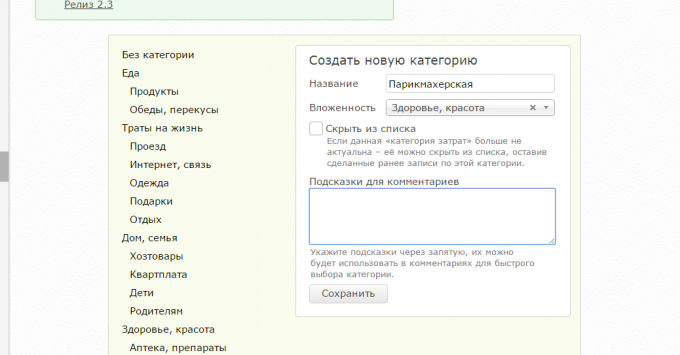

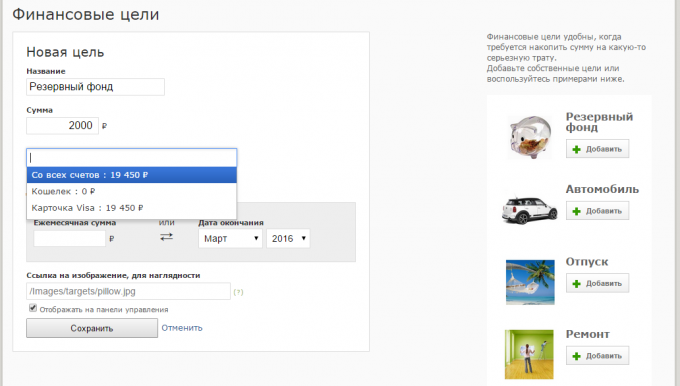

Immediately after registration you fill out a short form, the data from which will be useful to create a list of categories and basic recommendations. Ibid you immediately report the "safety cushion", which it is desirable to accumulate in the near future.

You can synchronize your account with bank cards of some Russian banks, including Sberbank, VTB, and others, and download transactions directly.

In addition, there is the financial condition of the indicators according to which the program will automatically give you a clue about the conduct of finance.

This service is very simple. There are no large analytical capabilities (there is an analysis of the annual cash flow) and synchronization with the banks, but it is not necessary to deal in anything. Service Provide you start coaching, you make your first transaction, and voila!

Create a budget, set goals for savings (already have a ready-made goals such as a vacation or "safety cushion", a click - the goal is added), add revenue and expenditure.

My Mind On My

There are all of the same income, expenses, and move between accounts. Income and expense categories are added in a separate section "References", and not just when entering transactions. But there are templates for frequently recurring expenses, which is quite convenient.

Budget planning and financial goals, big or medium, you need a premium account. However, such an account exists in any of the above programs, and without it you will get a minimum of possibilities.

What is good, from any of these Web services have mobile apps for iOS and Android, because enter your expenses from your mobile device is much easier.

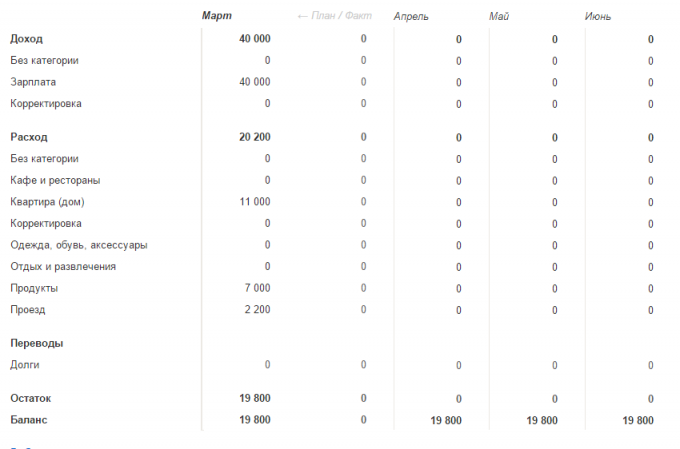

The first thing to do after creating your account - plan your budget. If you are officially certainly you get paid twice a month, and all taxes are already deducted from it. So just enter the amount of wages.

Then fill in your budget every month for recurring expenses, such as payment for an apartment, travel, internet and so on. It may be debt on the loan, child care, the amount that you necessarily are giving the elderly parents and other expenses that are clearly repeated month after month.

Now you can see a graph of your budget: how much you want to spend on different categories, as is already spent and how many will be able to spend more, not a loose budget.

You can create a separate category of "Everything else" or "just in case". There will be kept the money that you had not planned to spend according to your budget. So you will have a more accurate idea of how much there is free money for contingencies.

From planning the budget is much more convenient to use credit cards for cash-strapped period when you have already spent last salary, but an advance has not come yet, but soon will be.

The program is prescribed, how much money you have and what date it is necessary to pay. So you will not forget to make a payment, and you will not have to pay interest.

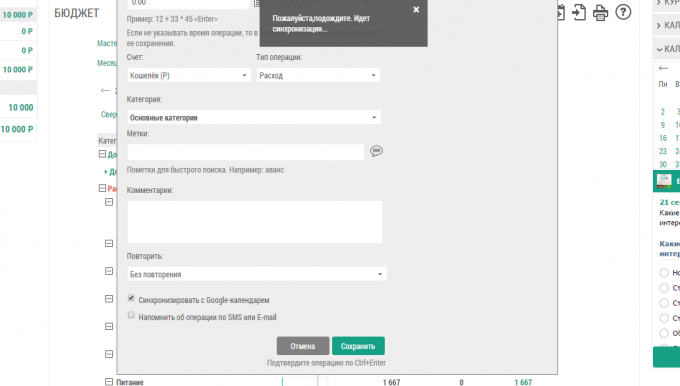

The Easy Finance for this purpose a special feature - automatic payments dates in Google Calendar, as well as reminders via email and SMS.

The "Zen-mani" also have such an opportunity, but without Google Calendar. You can schedule recurring transactions and advance receive reminders about them by email.

So you make a budget, and your expenses for a month stay within that budget. Ok, it's time to think about savings. You can also customize a service so that every month a certain amount is transferred as savings on your bill.

Excellent goal for saving - the "in case of emergency." This account will give you what we have to provide the money - security.

You decide how big are your savings, but more often than is recommended to postpone the sum, which in case of emergency will last for six months of life without work. If you are already a few months leads home accounting, this would be quite simple: take your average actual budget for the month and multiply the number by six.

When this amount is accumulated, do not touch it until the most extreme case like that you'll be out of a job, car or property. You'll see, with a reserve of money "just in case" you will feel much more comfortable, safer and more confident.

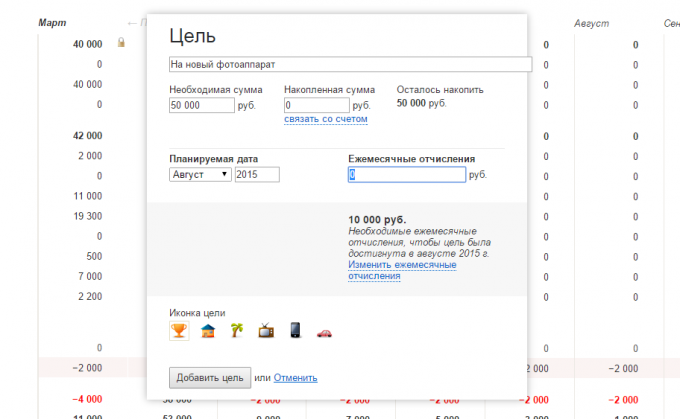

You can set other goals for accumulation. It may be different purchases, major or not, "selling Fund" savings for the coming vacation or something else.

If you calculate the budget, you can clearly understand how much money you can save for a thing, event or vacation every month.

For example, you see that each month in excess of the budget and general expenses have remained 5000 rubles. You can set a goal, such as "buy a new smart phone," and the program will calculate how much you need to save each month to accumulate the required amount, say, the end of summer. As a result, you get peace of mind and clarity in personal finance.

And you plan personal finances? What use tools?